Homeowner Alert: Time Limits for Filing Roof Insurance Claims in North Carolina

Blog

5 MIN READ

SHARE:

Homeowner Alert: Time Limits for Filing Roof Insurance Claims in North Carolina

When a weather event like a summer thunderstorm rolls through Asheville or a hurricane sweeps across the Carolina coast, your roof takes the brunt of the damage. Homeowners know this reality all too well — our state faces hurricanes, severe thunderstorms, hail, and high winds that can damage roofs in an instant. What many don't realize is that the clock starts ticking the moment that damage occurs and policyholder urgency is required.

Missing a roof insurance claim deadline can mean losing up to thousands of dollars in coverage, leaving you to pay for emergency repairs out of pocket. Insurance claim timelines aren't always straightforward, policy requirements often differ from state law, and discovering hidden damage months later adds another layer of complexity. Understanding the state laws and time limits for filing roof insurance claims protects you from missed deadlines, retains your financial protection against costly claim denials and helps you act confidently when storm damage strikes.

What Your Policy and North Carolina Law Say About Your Insurance Claim Period

Homeowners dealing with roof damage need to consider both their insurance policy clauses and state legal requirements. Most policies require an immediate written notice of loss, but what qualifies as immediate varies significantly between carriers. Some policies interpret this as 24-48 hours, while others accept notification within a reasonable time frame after discovering damage.

Your policy's proof of loss requirement triggers the insurer's investigation timeline. The North Carolina Department of Insurance mandates that insurers acknowledge claims within 30 days and complete investigations within 30 days after receiving proof of loss.

Beyond policy deadlines exists North Carolina's statute of limitations. State law provides three years from the date of loss to file a lawsuit against your insurer if they deny coverage. This statute of limitations cannot be shortened by policy language, and any insurance contract attempting to impose a shorter limitation violates NC legal requirements, and those specific provisions are void.

The discovery date matters in hidden-damage scenarios. When roof damage isn't immediately visible — such as hail storm impacts that only manifest as leaks months later — the timeline calculation becomes more complex. While your insurer expects prompt notification once you discover the problem, the three-year statute of limitations typically begins at the actual date of loss, not when you found it.

How Long You Have to File Roof Claims

Most NC standard claim windows fall within 30-60 days after damage occurs for initial notification. This claim filing period is the most common across carriers, but individual policies can have significant variations in actual requirements. It's essential that you read your policy documents carefully to understand what your carrier requires.

The following roof damage claim rule variations stem from different carrier policy types and coverage levels:

1-year limit: Some carriers enforce this time frame for certain types of gradual-damage claims, particularly for issues such as slow leaks or wear-related problems.

2-year limit: Other policies extend to this window for specific perils, depending on the coverage type and circumstances.

5-year limit: Certain commercial policies or specialty coverage may allow this extended time frame depending on the contract terms and circumstances.

How Catastrophic Events Can Impact Deadlines

North Carolina hurricane and storm claims often receive special consideration after catastrophic events. When major storms strike — like Hurricane Helene in 2024, which caused $59.6 billion in damage and affected 4.6 million residents across 39 counties — the state may issue emergency declarations. These declarations can extend standard filing deadlines, giving overwhelmed homeowners additional time to get federal disaster relief, assess damage, and file disaster claims. The volume of claims after a storm can also mean insurers face increased operational pressure, potentially delaying your claims processing.

Note that your deadline to report damage is not the same as the insurer's response deadline. To retain your roof damage protection, your homeowner responsibility is reporting damage promptly per your policy terms, which is typically far sooner than the insurer's internal processing timelines. Additionally, the deadline to file a claim or notify your carrier is likely much sooner than the deadline for the legal right to sue.

The Consequences of Missed Deadlines

As big storms are becoming more common, insurers are trying to preserve their profit margins by using denials to cut claim payments. When homeowners miss their policy's reporting deadline, insurers may view this as a policy breach. While not all deadline breaches lead to automatic denials, if you fail to meet contractual obligations, your insurance carrier may have grounds to deny coverage entirely, even if your claim is valid. This coverage forfeiture means losing your right to compensation.

The immediate impact hits homeowners as a significant financial burden. Out-of-pocket expenses can vary widely depending on the amount of damage, home size, material, and labor costs.

The Department of Insurance's dispute process and assistance can offer recourse if your claim is denied. You can request a written explanation, and insurers must provide this within 30 days under state regulations — then file an internal appeal with your carrier. If internal appeals fail, legal recourse remains available if you believe they are acting in bad faith and unfairly denying your claim. Legal counsel will help you understand the laws governing unfair insurance acts in NC.

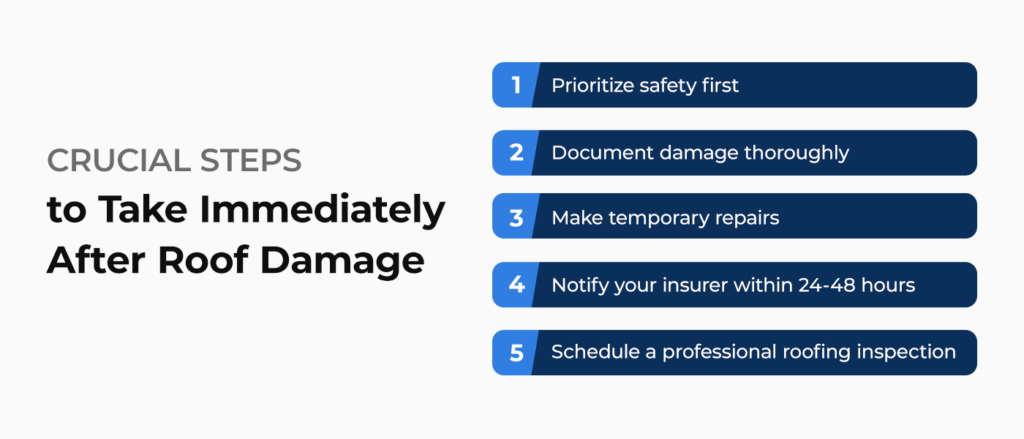

Crucial Steps to Take Immediately After Roof Damage

The moment storm damage occurs, taking the following immediate action protects both your home and your insurance coverage:

Prioritize safety first: Check for structural hazards like sagging ceilings, exposed electrical wiring or downed power lines before inspecting damage. Safety precautions protect you from injury during assessment.

Document damage thoroughly: As soon as it's safe, take photos and videos from multiple angles, capturing both wide shots showing overall roof condition and close-ups of specific problems like missing shingles, visible dents, cracked tiles or punctures. Photograph interior damage, including water stains, ceiling discoloration and active leaks. Create detailed records noting the date and time of the weather event, the type of storm and any immediate visible damage.

Make temporary repairs: Cover exposed areas with tarps, secure loose materials, and address active leaks to prevent further damage. Keep every receipt for emergency supplies and temporary fixes, as most policies reimburse these mitigation expenses. NC weather considerations make this urgent, as our hurricane season runs from June through November, and severe weather can compound existing damage quickly if left unaddressed.

Notify your insurer within 24-48 hours: Contact your insurance company as soon as you discover damage, even before you know the full extent. This prompt notification starts the clock on the insurer adjuster's investigation timeline.

Schedule a professional roofing inspection: Work with a company familiar with the state's rules. Expert roofers identify hidden damage that untrained eyes miss, such as granule loss on shingles, subtle hail impacts or windstorm damage to flashing and underlayment. Their comprehensive documentation and helpful policy review strengthen your claim and provide accurate information about repair needs and costs.

Ensure you understand local requirements and seek help if needed. Local laws affect your claim process as well as building codes, permitting requirements for repairs, and contractor licensing regulations, all of which play roles in legitimate insurance claims. If you face claim denial or complex coverage disputes due to a lack of insurance agent advice, consider legal consultation to protect your policyholder rights.

Act Fast and Be Informed to Protect Your Home

Understanding North Carolina's insurance claim filing deadlines, like knowing the difference between date of loss and date of discovery, is the first step, and you don't have to navigate the claims and appraisal process alone. Timely claim filing, thorough documentation and expert guidance make all the difference between your insurance policy's approval and denial.

Lifetime Quality Roofing and Exterior Services brings decades of experience helping homeowners protect their insurance coverage after filing a claim for storm damage. Our team understands the confusion surrounding policy language, claim deadlines and North Carolina-specific regulations. From comprehensive roof inspections that identify hidden and otherwise undetected damage to detailed reporting that strengthens your claim and tips for weather preparation, we partner with you every step of the way.

Schedule your free consultation with Lifetime Quality today, and gain the peace of mind that comes with expert support and policy knowledge throughout your insurance claim process.